The Russian Contagion Spreads to Belarus – Belarus Economy Digest

Belarus's GDP growth managed to strengthen in November. But despite this, many signals about an upcoming downturn have appeared. The Russian economic contagion began to spread to Belarus through trade and informational channels.

The government reacted by introducing a de-facto 30% devaluation that was accomplished in a rather ‘creative’ manner. But this decision seems to be more like a short-term relaxation than anything else, while further adjustments have become inevitable.

Real Economy: Output Strengthened, Prospects Worsened

In November, the growth rate for Belarus's output increased and reached 1.7% (standing at 1.5% in four previous months). However, the marked improvement in the dynamics surrounding the GDP dynamics will not become a sustainable trend.

First of all, this acceleration in November was mainly due oil-refining and the production of potash fertilisers. Both these and other industries associated with natural resources have utilised roughly all their available capacities. So, further output spurts by these industries is highly unlikely.

Second, a majority of other industries demonstrated either stable or negative dynamics with regards to their output. Output in non-manufacturing industries – construction, agriculture, trade, transport and communications – did not exhibit any substantial change. In manufacturing, there are some positive movements peculiar mainly to smaller industries, whose contribution to GDP is negligible.

Large industries – those that manufacture food products, non-metallic mineral products, basic metals, electrical equipment, transport vehicles – saw their performance worsen in November. A slowdown in these industries deepened, and at the same time a majority of them faced a growing volume of finished products inventories.

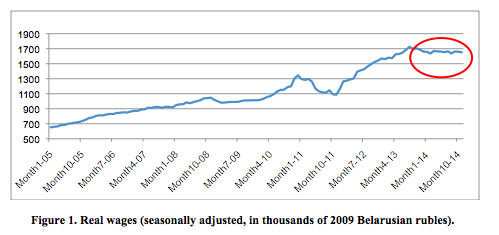

These negative trends mirror poor domestic and external demand. Domestic consumer demand is weakening because of stagnating real wages (see Figure 1). A majority of firms have to freeze or to cut wages in order to enhance their competitiveness.

Domestic investment demand is developing in a rather chaotic manner. In previous months it seemed to revive on a backdrop of lowering interest rates and government’s stimulation. However, in November this trend was reversed and a slowdown in capital investments began to be visible. The latter seems to be associated with the deterioration in business’ expectations and confidence.

Furthermore, many firms suffer from the ablation of working capital, which restricts their possibilities and propensity to finance investments through their own funds. Finally, banks tightened their credit supply in the current uncertain environment with its corresponding growing risks.

The external environment is the largest headache for Belarusian producers. Only businesses associated with natural resources (oil products, potash fertilisers, etc.) can rely on a stable level of demand. Other firms that operate on competitive markets are in state of perplexity.

The majority of Belarusian exporters produce capital goods for the Russian market. For their part, Russian agents have radically cut their investment expenses, given the start of the recession and the poor prospects of the Russian economy. Thus, new orders for Belarusian goods have dropped substantially.

problems with settlements on the supplies have already taken place Read more

Furthermore, there are signals that problems with settlements on the supplies have already taken place. For instance, in November incoming export payments decreased significantly in comparison both to October 2014 and November 2013. Moreover, external overdue debtor indebtedness seems to have begun to rise. Hence, there is a danger of massive payment defaults, which may further hamper the solvency of Belarusian enterprises.

In December, new challenges became visible for Belarusian producers. First, the signs of recession in Russia became more and more evident. Hence, the challenges of contracting demand and progressing instances of non-payment might have proliferated. Second, the mix of political and economic considerations pushed the Russian authorities to initiate a new “trade-war” with Belarus.

the statistics for December (when available) will record a huge drop in exports and revenues from Russia Read more

They accused Belarus of supplying prohibited goods from Western countries to Russia. Later this accusation transformed into a ban on the export of Belarusian meat and some other food products to Russia, which was formally listed as being due sanitary safety considerations. Hence, one may expect that the statistics for December (when available) will record a huge drop in exports and revenues from Russia. These hardships are directly affected by the currency market in December, which has become a first victim of the Russian spreading economic contagion.

Monetary Environment: Belarus Tries to Resist the Russian Currency Crisis

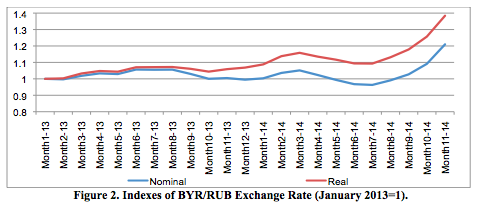

The contracting capacity of Russian markets developed alongside the gradually lowering price competitiveness of Belarusian producers. Until recently, the Belarusian authorities preferred to ignore the substantial appreciation of Belarusian ruble vs. Russian ruble, justifying it through considerations of their own domestic financial stability. This led to huge losses in the real price competitiveness of Belarusian producers on the Russian market (by roughly 30% in comparison to an average level of 2013 and the beginning of 2014, see Figure 2).

In a broad sense, one may argue that already in December a huge fraction of Belarusian firms have become uncompetitive on Russian markets.

Besides through trade channels, the Russian financial contagion began to spread via informational channels as well. Expectations of an inevitable depreciation followed. Correspondingly, Belarusian households and firms increased their demand for hard currency.

For instance, November has become the first month of the year when households became a pure purchaser of hard currency (some purchases on a net basis took place also in May, but it was close to zero). Furthermore, many households changed the currency of their deposits to US dollar (or other hard currencies besides the Belarusian ruble). This led to a quick depletion of international reserves (in November official international reserves shrank by USD 204m and total international reserves shrank by USD 460m).

Belarusian households began buying of hard currency in a panic Read more

In December, the currency panic in Russia (15-16 December) strengthened these ‘pure contagion’ channels. Belarusian households began buying of hard currency in a panic (according to the unofficial statements of the authorities, households purchased several hundred million dollars during four days). Finally, the Belarusian authorities were forced to react.

On the one hand, they intended to avoid the rapid depreciation or a one-shot devaluation, because they fear that such policy measures may become a trigger for a inducing mass panic on the deposits market. On the other hand, they were not ready to sell off a huge part of their international reserves.

On 19 December they decided to introduce a 30% commission for purchasing hard currency for all agents. Later on, they devaluated official exchange rate by roughly 10% and reduced the commission down to 20%. These measures mitigated the panic at the currency market somehow, but they have not solved their fundamental problems.

In fact, by taking these measures the authorities reserved some more time to think about their future policies and wait for more certainty vis-a-vis the Russian economy and the Russian currency market. However, the choices available to the authorities has seen a sharp narrowing.

The de-facto devaluation of the Belarusian ruble by 30% is still far from its equilibrium level. Hence, they should either depreciate the ruble further to a significant degree, or radically adjust domestic demand (i.e. sacrifice output dynamics and real wages), or finance any further disequilibrium with new borrowing.

Dzmitry Kruk, Belarusian Economic Research and Outreach Center (BEROC)

This article is a part of a joint project between Belarus Digest and Belarusian Economic Research and Outreach Center (BEROC)

Belarusian Diplomacy in 2014: Laying the Groundwork for 2015?

Lukashenka and Poroshenko in Kyiv

In 2014, Belarus lost its title as Europe's last dictatorship and Minsk offered up its name for the peace process in Ukraine. Belarus' self-inflicted isolation from the international democratic community has been seriously eroded but not definitely broken.

Belarus' response to the Ukrainian crisis helped to jump-start a promising positive trend in the country's relations with the West. Belarusian diplomats were very busy talking with their European colleagues. However, they mostly neglected other regions such as Africa.

Sympathising with Ukraine

Belarus' balanced position on Ukraine has become the country's biggest foreign policy success in 2014. It helped the Belarusian authorities to win the genuine appreciation of most Ukrainians and improve the regime's relations with the West.

Lukashenka refused to recognise the legitimacy of annexation of Crimea and the Russian-backed separatist authorities in Donetsk and Luhansk. He never hesitated when it came to publicly recognising or meeting with Ukraine's new authorities.

The latest meeting between Lukashenka and Ukrainian President Poroshenko took place in Kyiv on 21 December. The Belarusian leader promised "any support" to his counterpart "within 24 hours". Both parties emphasised economic and trade cooperation, which suffered because of the crisis.

The Ukrainian crisis made Belarus reassess its geopolitical situation Read more

However, Belarus carefully avoided alienating Russia on this issue, which would endanger the country's economic interests. To please Moscow, Lukashenka has often criticised the West's anti-Russian sanctions and NATO's increased military presence in neighbouring countries.

The Ukrainian crisis made the Belarusian authorities reassess the country's geopolitical situation. They no longer designate the West as the only threat to Belarusian sovereignty. Meeting with his ambassadors in July, Lukashenka unambiguously placed Russia among the global players whose soft power Belarus would have to withstand and counter.

Normalising Relations with the West

The EU and the US appreciated Belarus' contribution to peace-building efforts in Ukraine, which resulted in the worldwide-known "Minsk Protocol". This led to intensification of the dialogue between Belarus and the West.

However, Minsk and Brussels made the first resolute step towards improving their relations prior to the crisis, in February. They agreed then on starting the interim phase of the dialogue on modernisation. In 2014, the diplomats met four times in this format, mapping out the best form of future cooperation.

In 2014, Belarus and EU countries held several dozen bilateral events at the level of foreign ministers and their deputies. These included working visits, political and consular consultations, meetings between trade commissions and encounters on the margins of multilateral events with most EU countries. The most active contact was established with the Visegrad Four as well as Lithuania and Austria.

In general, contact at the highest level remained a taboo. However, the Ukrainian crisis provided Lukashenka with the opportunity to have a phone conversation with Polish Prime Minister (and future EU President) Donald Tusk and a Minsk visit for three senior EU commissioners.

Belarus is rapidly getting rid of its pariah status in Europe Read more

Minsk also became actively involved in the workings of several European multilateral forums, such as the Eastern Partnership and the Central European Initiative. Belarus has been determined to reformat the Eastern Partnership to have it better reflect Minsk's priority agenda with regards to European integration – less emphasis on human rights and more economic assistance and trade cooperation.

Judging by the quantity and quality of its working contacts, Belarus is rapidly getting rid of its pariah status in Europe.

The progress in Belarus' relations with the US has been much less noticeable. The two countries have liaised mostly on the middle diplomatic level. They have focused on international security issues but also discussed the economy and education.

Recently, some mass media has tried to sensationalise a statement on Belarus made by Victoria Nuland, US Assistant Secretary of State. In fact, answering a question from a Belarusian blogger on 18 December, she said that the US "remain[ed] open to a warmer, more integrated relationship with Belarus as the human rights situation improves".

Nothing indicated a policy change there. Victoria Nuland went on to emphasise that it was "in the hands of the [Belarusian] leadership whether they want[ed] to take their country in a more democratic, open direction".

Besides some signs of improvement in relations – quite promising with Europe and more timid with the US – one can hardly expect a major breakthrough before Belarus decides to do away with the outstanding issue of political prisoners.

Exploring the Third World

Guided by Lukashenka's instructions to open new markets for Belarusian goods, the foreign ministry tried hard to expand its ties with developing countries. In 2014, they focused on Latin America as well as China and South East Asia. Belarus exchanged high-level visits with several countries from these regions and opened embassies in Mongolia, Ecuador and Pakistan.

Africa got much less attention. Foreign Minister Vladimir Makei's visits to Nigeria and South Africa were Belarus' most notable activity on the continent.

Belarus is still underrepresented in the developing world Read more

Lukashenka's visit to the UAE in October received a lot of media fuss in Belarus. However, nothing appears to suggest that Minsk and Abu Dhabi are on the verge of a major upgrade in their ties. In the Middle East, Belarus also tried to revive ties with Iran and Iraq and maintain them with war-torn Syria.

Belarus is still diplomatically and economically underrepresented in the developing world. Much more resources need to be invested to penetrate these markets with Belarusian goods on a sustainable basis.

Lacking New Attractive Ideas in Multilateral Diplomacy

In 2014, the United Nations' system remained Belarus' preferred tool for promoting its foreign policy initiatives and a source of development assistance.

Belarus' three key initiatives has been the fight against human trafficking, the protection of 'traditional family values' and the prohibition of the development and manufacturing of new weapons of mass destruction.

No international consensus on Belarus' newest multilateral initiative Read more

It is unlikely that Belarus will continue to earn as many diplomatic points on the fight against human trafficking as it used to in recent years. The prospects of the other two initiatives seem to be rather bleak.

Belarus vehemently defended its conception of a traditional family at every occasion at the UN. However, this initiative has failed to gather international support. Most nations oppose Belarus' views on same-sex marriages or are at least indifferent to this issue.

As for Belarus' efforts to prevent the emergence of new WMDs, the current tensions among the great powers seriously undermine them.

In 2014, Belarusian diplomats succeeded in organising visits by the heads of UNDP and UNESCO to Minsk. UNDP Administrator Helen Clark's visit became a true achievement for Belarusian diplomacy. It helped to re-emphasise Belarus' need for international assistance in overcoming the aftermath of Chernobyl.

Understanding Priorities for 2015

In 2015, the Belarusian diplomats will focus on two priorities.

First of all, Lukashenka expects them to open new markets for Belarusian goods in order to prevent Belarus from being further sucked in the Russian economic crisis. However, the foreign ministry lacks the proper tools and resources to be able to influence foreign trade to a significant extent.

Second, Belarusian diplomacy must ensure international acceptance and recognition of Lukashenka's re-election to the country's highest office. Their success in doing so will largely depend on the degree of political liberalisation the Lukashenka will agree to tolerate.