Output Grows, but Inflation Hurting Macroeconomic Stability – Digest of Belarusian Economy

The economy of Belarus is showing signs of rising levels of output with most industries increasing their overall output figures throughout May. At the same time foreign and domestic investment demand are exhibiting signs of recovery.

However, this recovery does not itself necessarily signal a return to high output growth. The growth rate is likely to remain weak in the coming months and a new challenge – climbing inflation – might hurt the economy.

Output: Growth is Reviving, but Remains Poor

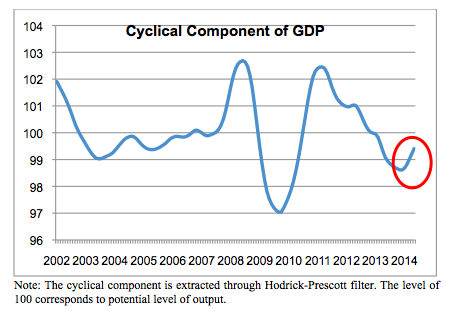

The Belarusian economy has entered a period of recovery (see Figure 1). Belstat reported that in January-May output grew by 1.5% (0.5% in the 1st quarter, and 1.1% in January-April). Indeed, broad positive trends in output have become more systematic and noticeable.

On the production side, major industries displayed gradual output growth across different sectors (trade, manufacturing, agriculture, electric power production) in May. Only construction and a number of manufacturing sub-industries (mainly machinery and equipment manufacturing) seem to be exceptions to this general trend.

On the demand side, an increase in investment activity and on external markets set the stage for recovery. External factors have also played an important role in Belarus' economic revival through May. In particular increased potash fertiliser exports, having recovered after demand was driven down in 2013, has become one of the most notable changes. Consumer activity remained strong, although its growth is likely to weaken in the near future due to real wages stagnating.

Despite a number of encouraging trends in the real economy, in general the overall economy's prospects have not significantly improved. Several factors are hampering its growth. First, its poor growth potential remains one of Belarus' core issues. Even according to the most optimistic forecasts for 2014, the GDP's growth rate will remain extremely modest (up to 3% by the end of the year).

Second, financial markets and the monetary environment continue to be in a very fragile state. The authorities achieved some success in making them more stabile and reducing interest rates over the past couple of months. However, they will hardly succeed in sustaining it if another shockwave ripples through the economy, especially if they fail to find a way get access new foreign loans.

Should things start to fall apart, the authorities will have to tighten their interest rate policy against a backdrop of growing inflation. However, if they are able to continue to build momentum for sustained domestic investment, which has been successful thus far thanks to reduced interest rates and increased liquidity in the banking system, they might be able to reverse this negative trend.

Third, a contraction the volume of intermediary imports has had an enormous impact on improving the environment of the nation's net exports. However, there are doubts about the origins of this shift (i.e. was it driven by the preferences of firms or was it the outcome of an administrative restriction being placed on imports) and its sustainability (i.e. can firms maintain their current levels of production if they receive fewer imported intermediate inputs).

Monetary Environment: The Threat of a New Inflation Spike

In 2013, the inflation rate steadily fell, reflecting a gradual shift in inflation forecasts (which, nevertheless, remained high and volatile), contracting domestic demand for investment and a relatively strict economic policy. Growing inflation appeared to be relatively consistent in 2014, as the majority of the factors that contribute to it persisting in the economy.

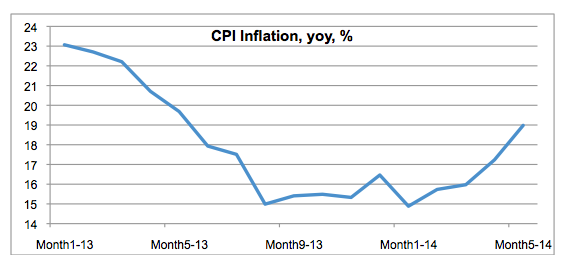

However, recently the situation appears to have changed. Since the beginning of the year the rate of inflation has began to gain momentum with the annual CPI (consumer price index) inflation rate reaching 19% (see Figure 2) in May.

Administratively regulated prices for services are the main culprit. Since the beginning of the year the tariffs on utilities and transportation have grown considerably (by 20.6% and 15.5% correspondingly). In reality, raising these tariffs is sound policy, and despite the opaqueness of how the new rates were reached, it was necessary to adjust them to a more fiscally responsible and economically reasonable level.

Another contributing factor has been the government's decision to dealing with the Belarusian rubles exchange rate. Given its lack of access to external financing, along with a huge deficit of current account, they could not avoid employing this tool for mitigating the nation's currency deficit. A more rapid pace for depreciation also contributed to prices going up.

There was also a significant spike in foodstuff prices in 2014 (up 12% since the beginning of the year). Meat prices (particularly pork prices) lead the pack in terms of growth. Prices for meat and poultry grew by 25.3% from January-May, with pork jumping 51.0%.

A substantial reduction in the nation's pig stock (due to an outbreak of African hog cholera in 2013) the primary driver behind this trend. Still, trying to explain the sharp jump in foodstuff prices in terms of African hog cholera alone seems to be misleading.

In 2014, agriculture's growth rate of costs has been considerable, making it among the leading industries of the economy. In the 1st quarter, expenses in this sector grew 25.4%, while the average rate of expenses throughout the economy was just 10.6%.

Such a pronounced growth in costs cannot be explained away by African hog cholera. The low levels of efficiency witnessed throughout agricultural sector as a result of large direct and indirect subsidies to it may provide a better explanation, or at least an alternative one, for rising costs and the subsequent price adjustments.

A new round of inflation rate hikes has developed into a serious potential threat for the national economy. Read more

A new round of inflation rate hikes has developed into a serious potential threat for the national economy. Accelerating inflation may drive up expectations about its future direction. Alternatively, increased inflation expectations may lead to a new wave of deposits being tied to dollars. If this is the case, the authorities will have to enforce a strict interest rate policy in order to cease deposits being done in dollars, which would result in additional output losses.

Furthermore, a sharp spike in prices for a small group of goods and services (especially intermediate goods like fuel and utilities) may distort the structure of relative prices and correspondingly cause adjustments in other prices to eliminate these distortions.

Finally, increasing prices will lead to less a lower level of competiveness for the Belarus' producers and manufacturers. In battling to fend it off, it may become clear that a rapid pace of depreciation will become necessary. However, given the closer relationship between exchange rates and prices, the threat of a new inflation-depreciation downward spiral may arise alongside output losses.

Dzmitry Kruk, Belarusian Economic Research and Outreach Center (BEROC)

This article is a part of a joint project between Belarus Digest and Belarusian Economic Research and Outreach Center (BEROC)

Belarus Produces More Refugees than It Saves

According to the United Nations, over 54,400 people have been displaced internally by the conflict in Ukraine. The ongoing turmoil raises the possibility that some Ukrainians will seek refuge in Belarus.

President Alyaksandr Lukashenka promised to support any and all Ukrainians in need. However, to date, only 65 Ukrainians have applied for refugee status in Belarus, a small number when compared to the 9,500 Ukrainians seeking official refugee status in Russia.

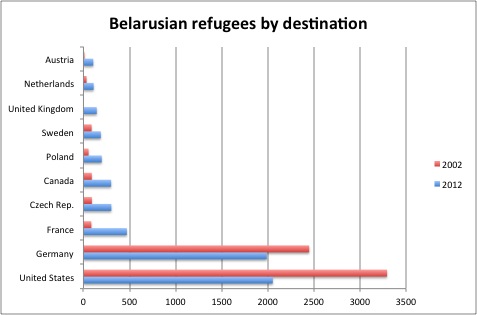

Despite its relative political stability, only about 891 people have obtained official refuge status in Belarus in 2014. In contrast, over 6,000 Belarusians hold refugee status abroad. To date, the Belarusian regime has blithely encouraged its political opponents to leave the country. And so they did, along with a great number of others who left for economic, rather than, political reasons.

As a result, Belarus is losing swathes of its politically or economically active citizens, people who are far less able to bring about positive socio-economic changes from abroad.

Who Seeks Refugee Status in Belarus?

Every year, about 200 people seek refugee status in Belarus. Over the years, most asylum seekers have come from Afghanistan. Since 2013, however, the number of Syrian refugees has increased. In the past, Belarus also hosted refugees from Georgia.

Most refugee seekers come from countries involved in warfare or ethnic conflict. The open Russia-Belarus border, on the one hand, and the construction of a common external border around the EU member states, on the other, have contributed to an increase in the number of refugees coming from Asia to the EU.

Belarus and other post-Soviet states on the EU border are increasingly becoming home to the EU’s unwanted migrants. When apprehended on the EU border, migrants often apply for refugee status in Belarus in order to avoid prosecution for illegal border crossing.

Belarus complies with the international refugee regulations and has acceded to the 1951 Geneva Convention and the 1967 Protocol. While Belarus has no refugee camps, several temporary accommodation centres are available. After seven years living in country, refugees can apply for Belarusian citizenship, provided they know one of the state languages and respect its national legislation.

Since 1997, over 3,000 people from 33 countries have applied for refugee status in Belarus. For every refugee approved, there are about 3 denials. The acceptance rate is thus much higher than in many other countries. The international average for granting asylum is a mere 3-7% of all applicants. While on paper all foreigners have the right to seek asylum, the Belarusian authorities reportedly decline asylum requests from Russian citizens.

Perhaps one of the most notorious characters sheltered by the Belarusian state is the deposed president of Kyrgyztan, Kurmanbek Bakiev. In 2010, during the upheaval in Kyrgyzstan, Kurmanbek Bakiev’s security forces fired on protesters, killing 40 and wounding 400. Bakiev is accused of committing mass murder back home, yet was welcomed as a guest and friend by the Belarusian President when he arrived at the Minsk airport with four members of his family. By now he has allegedly become a citizen of Belarus.

Belarusians on the Run

Belarus produces its own share of asylum seekers, even though it is a relatively stable and peaceful affair. Many Belarusians seek protection due to the political situation in Belarus. There are also some cases of LGBT asylum seekers, who seek protection from persecution on the basis of their sexual orientation. And, of course, some people leave for economic reasons but find it more expedient to apply for political asylum than to try to go through other channels.

The number of Belarusians seeking asylum has peaked in the first half of the 2000s and been on a steady decline since then.

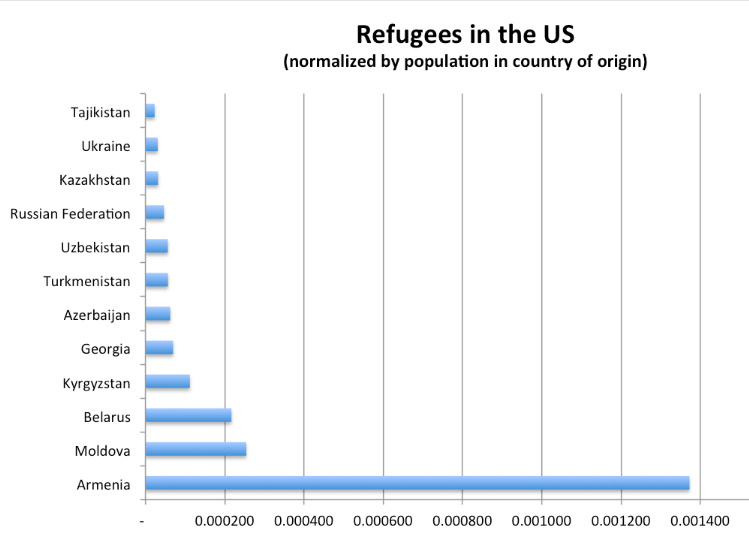

Even so, far more Belarusians are seeking asylum today than, for example, Kyrgyzstanis or Russians, when differences in the size of their respective populations are taken into account. Most Belarusians find asylum in the United States or Germany, two western counties that serve as the key destinations for over two thirds of all asylum seekers from Belarus.

Belarusians hold the dubious honour of becoming the first post-Soviet nationals to seek political asylum in the United States. In 1996, two prominent leaders of the democratic opposition – Zianon Pazniak and Sergei Naumchik – applied for asylum there. They said their lives were in danger and criticised the Belarusian government for persecuting the political opposition and controlling the media.

Belarusians hold the dubious honour of becoming the first post-Soviet nationals to seek political asylum in the United States. In 1996, two prominent leaders of the democratic opposition – Zianon Pazniak and Sergei Naumchik – applied for asylum there. They said their lives were in danger and criticised the Belarusian government for persecuting the political opposition and controlling the media.

Many other prominent Belarusians have obtained asylum abroad since then. For example, in 2011, Belarus Free Theatre founders Natalia Kaliada and Nikolai Khalezin won political asylum in the United Kingdom. The theatre has staged many controversial plays, both in Belarus and abroad, which emphasised important issues such as politically motivated disappearances, human rights violations, or the death penalty in Belarus.

In 2012, Andrei Sannikov, who came a distant second in the 2010 presidential election, received political asylum in the UK. When Sannikov’s wife, award-winning journalist Iryna Khalip, was visiting her husband abroad, the Belarusian authorities reportedly pressured her to permanently leave the country. To this day, she lives in Belarus.

Urging Belarusians into Exile, with Repercussions

These are just few well-known cases, but each year a large number of Belarusian political activists seek political asylum abroad. The Belarusian government does not prevent them from leaving, as they cause far less trouble abroad than they do at home. This is why Iryna Khalip may have been pressured to follow her husband into exile. President Lukashenka has on a number of occasions stated that Belarusian activists can easily leave into exile if they choose to do so.

While in the short term this approach may save activists from persecution, in the long run encouraging political activists to leave will weaken civil society, independent media, and the political opposition in Belarus. Whether there are any benefits to Belarus when its citizens seek political asylum abroad remains to be seen.

While in the short term this approach may save activists from persecution, in the long run encouraging political activists to leave will weaken civil society, independent media, and the political opposition in Belarus. Whether there are any benefits to Belarus when its citizens seek political asylum abroad remains to be seen.

So far, the political activists living in asylum abroad have spent too much energy warring with each other. Belarusian communities in exile remain divided as activists compete for victimhood status and fight over invitations from Western organisations. To promote their own names, they often accuse each other of making compromises or selling out to the regime.

In the end, the regime can successfully play off its opponents against each other even from far away. Ironically, the atmosphere that pervades the Belarusian political communities in the democratic West at times resembles the atmosphere of mutual distrust and accusations that were so pervasive in the Soviet Union.

European institutions face problems when working with this kinds of conditions. They cannot engage people who are in prison in Belarus and face diminishing returns when engaging exclusively with political refugees who can no longer travel to Belarus. Belarusians who remain at home have a significantly better ahcen of making a difference, but unfortunately they are often accused of working for the regime or making compromises.